Understanding the Settlement Check Process

Winning a legal settlement can feel like reaching the finish line of a marathon, but the reality is that receiving your money involves several more steps. Understanding the settlement check process helps set realistic expectations and ensures you’re prepared for what comes next. Whether you’ve won a personal injury case, employment dispute, or another type of civil litigation, the path from victory to payment follows a specific timeline with important milestones along the way.

The Victory Moment: What Happens Immediately After Winning

When a judge or jury rules in your favor, or when both parties sign a settlement agreement, you might expect a check to arrive within days. However, the legal and financial processes that follow take considerably longer than most people anticipate. The moment of victory marks the beginning of the settlement check process rather than its conclusion.

After winning your case, several parties must review and approve the settlement terms. Even in cases where you’ve agreed to a settlement before trial, the documentation requires careful examination by attorneys, insurance companies, and sometimes courts. This review process ensures that all terms are properly documented and legally binding before any money changes hands.

The Settlement Agreement: Dotting the I’s and Crossing the T’s

The first major step involves finalizing the settlement agreement or satisfaction of judgment. This legal document outlines every detail of the settlement, including the total amount, payment terms, and any conditions attached to the payment. Your attorney will review this document meticulously to ensure it accurately reflects the agreed-upon terms.

Settlement agreements typically include several key components. The payment amount appears first, but the document also specifies whether payments will be made in a lump sum or structured over time. It outlines any confidentiality clauses, non-disparagement agreements, or other conditions you must meet to receive payment. The agreement also includes a release of liability, meaning you agree not to pursue further legal action related to this claim.

Both parties must sign the settlement agreement before proceeding. If the opposing party is a large corporation or insurance company, this signature may need to pass through multiple levels of approval. Each layer of bureaucracy adds time to the process, though your attorney can sometimes expedite matters by maintaining regular communication with the opposing counsel.

Court Approval: When a Judge Must Sign Off

Certain types of settlements require court approval before you can receive payment. Cases involving minors almost always need judicial review to ensure the settlement serves the child’s best interests. The court may require that settlement funds for minors be placed in a structured settlement or blocked account that restricts access until the child reaches adulthood.

Class action settlements and some medical malpractice cases also require court approval. The judge reviews the settlement terms to verify they’re fair and reasonable given the circumstances of the case. This review process can take several weeks or even months, depending on the court’s schedule and the complexity of the case.

During the approval hearing, the judge may ask questions about how the settlement amount was calculated or why certain terms were included. Your attorney will present arguments supporting the settlement’s fairness. Once the judge signs the approval order, the settlement moves forward to the payment stage.

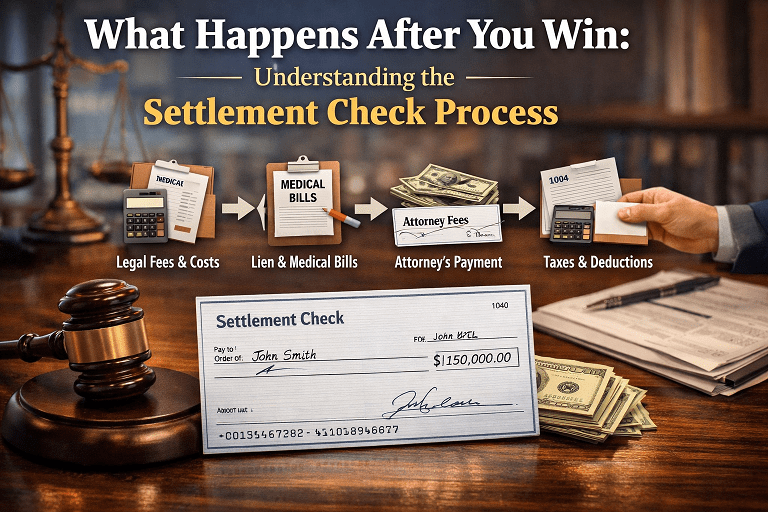

Attorney Fees and Cost Deductions: Understanding What You’ll Actually Receive

One of the most important aspects of the settlement check process involves understanding deductions. The settlement amount awarded or agreed upon is rarely the amount you’ll deposit into your bank account. Several deductions reduce your final payment, and knowing these in advance prevents disappointment.

Attorney fees represent the largest deduction from most settlements. If your attorney worked on a contingency basis, which is common in personal injury cases, they typically receive between 25% and 40% of the settlement amount. This percentage may vary based on when the case settled, with attorneys often receiving a lower percentage for cases that settle before trial and higher percentages for cases that go to verdict.

Beyond attorney fees, you’ll also repay legal costs advanced by your attorney during your case. These costs include filing fees, expert witness fees, deposition costs, medical record retrieval fees, and investigation expenses. Depending on the complexity of your case, these costs can range from a few hundred dollars to tens of thousands.

Medical liens represent another significant deduction. If you received treatment from healthcare providers who agreed to wait for payment until your case settled, or if your health insurance company paid for treatment related to your injury, these parties have a legal right to reimbursement from your settlement. Your attorney will negotiate these liens to reduce them when possible, but you must satisfy them before receiving your portion of the settlement.

The Payment Timeline: How Long Until You See Money

The timeline from settlement agreement to payment varies considerably based on several factors. In straightforward cases where no court approval is needed and all parties agree on the terms, you might receive payment within 30 to 45 days. More complex cases involving court approval, multiple defendants, or insurance company delays can extend this timeline to 60 days or longer.

Insurance companies typically issue settlement checks within 30 days of the settlement agreement being signed, though some policies allow up to 60 days. Large corporations may have similar timelines built into their payment processes. Government entities often have even longer payment windows, sometimes extending to 90 days or more due to bureaucratic procedures.

Your attorney’s office plays a crucial role in this timeline. When the settlement check arrives, it’s typically made payable to both you and your attorney or solely to your attorney’s trust account. This ensures that all liens and fees are properly handled before you receive funds. Your attorney must deposit the check, wait for it to clear (which can take 7-10 business days for large amounts), calculate all deductions, and then issue checks to all parties with valid claims against the settlement.

The Trust Account Process: Why Your Money Makes a Pit Stop

Settlement checks don’t go directly into your personal account because attorneys are ethically and legally required to handle settlement funds through their trust accounts. These special accounts separate client funds from the attorney’s operating funds and provide a clear paper trail for all transactions.

When your settlement check arrives at your attorney’s office, several steps follow in quick succession. The attorney deposits the check into the trust account and notifies you of its arrival. While waiting for the check to clear, your attorney’s staff prepares a settlement statement showing all deductions from the gross settlement amount.

The settlement statement itemizes every dollar. It shows the total settlement amount, attorney fees calculated according to your fee agreement, reimbursement for costs advanced during your case, and payment amounts for each medical lien or other claim against the settlement. The remaining amount represents your net recovery, the actual money you’ll receive.

Once the settlement check clears, your attorney disburses funds according to the settlement statement. Lienholders receive their payments, the attorney transfers their fees and cost reimbursements, and you receive a check for your portion. Many attorneys now offer electronic payment options that can speed up this final step, though some clients prefer traditional checks for record-keeping purposes.

Structured Settlements: An Alternative Payment Option

Not all settlements involve a single lump-sum payment. Structured settlements provide periodic payments over time instead of one large check. These arrangements are common in cases involving substantial amounts, long-term care needs, or minors.

Structured settlements offer several advantages. They provide guaranteed income over a specified period, which can be helpful if your injury requires ongoing medical treatment. The payments are typically tax-free, just like lump-sum personal injury settlements. Structured settlements also protect beneficiaries from spending their entire settlement too quickly, ensuring funds remain available when needed most.

The structure can be customized to meet your specific needs. You might receive monthly payments for living expenses, annual lump sums for major expenses, or a combination of both. Some structures include increasing payments to account for inflation, while others front-load payments during years when medical expenses are highest.

However, structured settlements come with drawbacks. Once established, you cannot change the payment schedule, even if your circumstances change dramatically. You cannot access the full settlement amount if an emergency arises. While companies exist that purchase structured settlement payment rights, they typically pay substantially less than the actual value of future payments.

Tax Implications: What You Need to Know

Understanding the tax consequences of your settlement helps you plan appropriately and avoid surprises at tax time. Generally, compensation for physical injuries or physical sickness is not taxable under federal law. This means if you settled a personal injury case for medical expenses, pain and suffering, and lost wages due to physical injury, you typically won’t owe federal income tax on that money.

However, certain portions of settlements are taxable. Punitive damages are always taxable, regardless of the type of case. Interest earned on settlement funds while they’re held in escrow or a trust account is also taxable. If your settlement includes compensation for lost wages in an employment discrimination case or emotional distress unrelated to physical injury, those portions may be taxable as ordinary income.

The settlement agreement should specify how the settlement amount is allocated among different types of damages. This allocation affects your tax liability, so work with your attorney to ensure the allocation accurately reflects the nature of your case. Consider consulting with a tax professional before receiving your settlement, especially if the amount is substantial or includes taxable components.

Special Considerations for Different Case Types

The settlement check process varies slightly depending on your case type. Personal injury settlements from car accidents, slip and falls, or medical malpractice typically follow the standard process outlined above, with medical liens being a primary concern.

Workers’ compensation settlements often involve approval by a state workers’ compensation board. These settlements may affect your eligibility for future workers’ compensation benefits, so understanding the long-term implications is crucial before signing any agreement.

Employment settlements require careful attention to tax withholding. Portions representing back pay or front pay are subject to employment taxes and withholding, while portions representing emotional distress may have different tax treatment.

Class action settlements involve unique procedures. Payment typically arrives months or even years after the settlement is announced, as claims must be verified and processed for potentially thousands of class members. Individual payments in class actions are often much smaller than in individual lawsuits.

Red Flags and Delays: When to Be Concerned

While some delays in the settlement check process are normal, certain situations warrant concern. If more than 60 days have passed since the settlement agreement was signed and you haven’t received any communication about payment, contact your attorney for an update.

Be wary if your attorney is uncommunicative or evasive about the status of your settlement check. Attorneys are required to keep clients informed about the status of their cases, including settlement payments. If your attorney fails to respond to reasonable inquiries, you may need to contact your state bar association.

If you receive your settlement check and the deductions don’t match what was explained to you earlier, ask for a detailed explanation. You’re entitled to a complete accounting of all deductions from your settlement. If your attorney cannot provide satisfactory documentation, you may need to seek advice from another attorney or report the matter to your state bar.

What to Do When Your Check Arrives

When you finally receive your settlement check, take several important steps to protect yourself and make the most of your recovery. First, verify the amount matches the settlement statement provided by your attorney. Check that all deductions were properly applied and that you understand every line item.

Deposit the check promptly, but be aware that banks often place holds on large deposits. Your bank may make only a portion of the funds available immediately, with the remainder becoming available after several business days. Ask your bank about their hold policies for large checks to avoid overdrawing your account.

Before spending your settlement, consider your long-term needs. If your injury has ongoing consequences, set aside funds for future medical care. Consider paying off high-interest debt, establishing an emergency fund, and meeting with a financial advisor about investing a portion of the settlement for long-term growth.

Keep detailed records of your settlement and how you spend the funds. Save copies of the settlement agreement, settlement statement, and your check. These documents may be important for tax purposes or if questions arise later about the settlement.

Moving Forward After Settlement

Receiving your settlement check marks the end of your legal case but the beginning of a new chapter. For many people, settlements provide crucial financial stability after a difficult period involving injury, job loss, or other hardship. Taking time to make thoughtful decisions about your settlement funds helps ensure this money serves its intended purpose.

Consider the emotional aspects of settlement as well. Closing a legal case can bring relief, but it can also stir up feelings about the incident that led to your case. Some people benefit from counseling or support groups as they process both the event and the conclusion of their legal journey.

The settlement check process, while sometimes frustrating in its complexity and length, exists to protect all parties and ensure proper handling of funds. Understanding each step helps you navigate the process with realistic expectations and confidence. When your check finally arrives, you can move forward knowing that every procedural requirement has been met and your settlement is secure.