Who Gets Paid From Your Settlement and In What Order

When you receive a personal injury settlement or jury award, you might assume that money is entirely yours to keep. Unfortunately, that’s rarely the case. Various parties may have legal claims against your settlement proceeds through what’s called medical liens. Understanding who gets paid from your settlement and in what order can help you set realistic expectations and avoid unpleasant surprises when it’s time to receive your compensation.

What Are Medical Liens?

A medical lien is a legal claim against your personal injury settlement or judgment that allows healthcare providers, insurers, or government programs to recover money they spent on your injury-related medical treatment. These liens ensure that entities who paid for your medical care can be reimbursed when you receive compensation from the at-fault party.

Medical liens can significantly reduce the amount of money you ultimately take home from your settlement. In some cases, liens can consume a substantial portion of your award, leaving you with far less than anticipated. That’s why understanding how these liens work and how they can be negotiated is crucial to maximizing your recovery.

Health Insurance Subrogation: Your Insurer’s Right to Repayment

One of the most common types of liens comes from your own health insurance company through a process called subrogation. When you’re injured in an accident, your health insurance typically covers your medical bills initially. However, most health insurance policies contain subrogation clauses that give the insurer the right to be reimbursed from any settlement or judgment you receive from the responsible party.

How Health Insurance Subrogation Works

Here’s how the process typically unfolds: You’re injured in a car accident caused by another driver. Your health insurance pays $50,000 in medical bills for your treatment. Later, you settle your claim against the at-fault driver for $150,000. Your health insurance company can assert a subrogation lien for the $50,000 they paid, meaning they want that money back from your settlement.

The legal theory behind subrogation is that you shouldn’t receive a double recovery for the same injury. Since your health insurer already paid your medical bills, allowing you to also collect for those same bills from the at-fault party would give you more than what you lost.

Types of Health Insurance Plans and Subrogation Rights

The strength of a health insurer’s subrogation rights depends largely on what type of plan you have:

ERISA Plans: If your health insurance is through an employer-sponsored plan governed by the Employee Retirement Income Security Act (ERISA), the insurer typically has strong subrogation rights under federal law. ERISA preempts many state laws that might otherwise limit subrogation, making these liens particularly difficult to reduce.

Private Health Insurance: If you purchased health insurance on your own or through a state exchange, state laws regarding subrogation apply. Some states have enacted laws that limit or eliminate subrogation rights in certain circumstances, particularly when the settlement doesn’t fully compensate the injured person.

Medicare Advantage Plans: These plans combine aspects of both government programs and private insurance, and their subrogation rights can be complex, often requiring specialized handling.

Hospital Liens: When Medical Providers Assert Direct Claims

Hospital liens represent another significant category of claims against personal injury settlements. Unlike subrogation liens where an insurer seeks reimbursement for payments already made, hospital liens arise when healthcare providers treat uninsured or underinsured accident victims and then place a lien directly against any future settlement or recovery.

How Hospital Liens Are Established

Most states have statutory provisions that allow hospitals and other healthcare providers to file liens against personal injury claims. When you receive treatment at a hospital following an accident, the hospital may file a formal lien notice with the county recorder’s office and provide notice to you and your attorney. This lien creates a legal claim against any settlement proceeds related to that accident.

Hospital liens typically cover emergency services, inpatient care, surgical procedures, and other medically necessary treatment directly related to your injuries. The lien amount equals the charges billed by the hospital, which are often significantly higher than what insurance companies would pay for the same services.

Challenges With Hospital Liens

Hospital liens present unique challenges because the amounts claimed are often based on the hospital’s standard “chargemaster” rates rather than negotiated insurance rates. A procedure that an insurance company would pay $5,000 for might appear on a hospital lien as $15,000 or more. This discrepancy creates opportunities for negotiation but also requires careful handling to ensure fair resolution.

Some states have enacted laws limiting hospital liens to reasonable and necessary charges or requiring hospitals to accept negotiated rates similar to what insurers pay. However, other states allow hospitals to claim their full billed charges, making negotiation more difficult but still possible.

Medicare and Medicaid Recovery Rights: Government Claims on Your Settlement

When government health programs like Medicare or Medicaid pay for your injury-related medical treatment, they have powerful rights to recover those payments from your settlement. These programs operate under federal law, giving them recovery rights that can be even more difficult to navigate than private insurance liens.

Medicare Secondary Payer Act and Conditional Payments

Medicare operates under the Medicare Secondary Payer (MSP) Act, which makes Medicare the “secondary payer” when another party is responsible for injuries. Under this framework, Medicare may make “conditional payments” for your treatment while your injury claim is pending. However, Medicare expects full reimbursement of these conditional payments when you settle your case.

Before you can finalize a personal injury settlement, you must report the settlement to Medicare and resolve Medicare’s lien. Failure to do so can result in serious consequences, including Medicare refusing to pay for your future medical care and potential penalties.

The Medicare recovery process involves:

- Requesting a conditional payment letter from Medicare showing what they paid

- Disputing any charges that weren’t related to your injury

- Negotiating the final reimbursement amount

- Obtaining a final demand letter

- Paying Medicare from the settlement proceeds

- Documenting the resolution

Medicare Set-Asides: Protecting Future Interests

In cases involving future medical expenses, particularly with significant settlements, Medicare may require a Medicare Set-Aside (MSA) arrangement. An MSA is a financial agreement that allocates a portion of your settlement to pay for future injury-related medical expenses that Medicare would otherwise cover. This protects Medicare from having to pay for treatment that your settlement should cover.

MSAs are particularly common in workers’ compensation cases but can apply to liability settlements as well. The amount set aside must be exhausted paying for Medicare-covered services before Medicare will begin covering those services again.

Medicaid Recovery and MERP

Medicaid operates under different rules than Medicare, with each state administering its own Medicaid program within federal guidelines. Medicaid recovery is handled through the Medicaid Estate Recovery Program (MERP), which seeks reimbursement not just from settlements but also potentially from the recipient’s estate after death.

When Medicaid has paid for your injury-related treatment, the state Medicaid agency must be notified of your settlement and given an opportunity to assert its lien. Like Medicare, Medicaid expects reimbursement from your settlement proceeds, though the specific rules and negotiation possibilities vary by state.

Many states have adopted more flexible approaches to Medicaid liens in recent years, recognizing that aggressive recovery can leave injury victims with little compensation for their pain and suffering. Some states apply formulas that reduce the Medicaid lien based on attorney’s fees and the extent to which the settlement compensates you for non-medical damages.

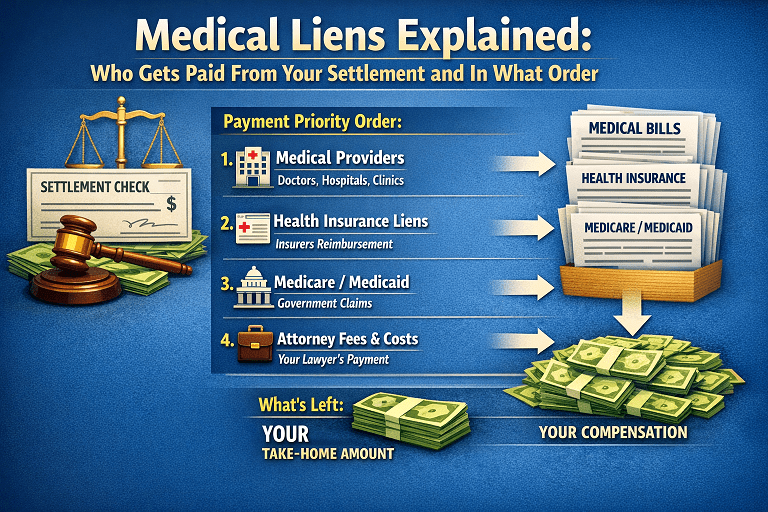

The Priority of Liens: Who Gets Paid First?

When multiple liens exist against a settlement, determining the order of payment becomes crucial. Generally, liens are paid in this priority order:

- Attorneys’ fees and costs: Your personal injury attorney’s contingency fee and litigation costs are typically deducted first

- Government liens: Medicare and Medicaid liens generally take priority over private liens due to federal and state law protections

- Hospital and medical provider liens: Statutory medical liens typically come next

- Health insurance subrogation liens: Private health insurance claims are usually paid after statutory liens

- Your recovery: Whatever remains after satisfying liens goes to you

However, this order isn’t absolute. State laws vary regarding lien priority, and the specific terms of insurance policies and agreements can affect the payment sequence. In some cases, negotiations result in pro-rata distributions where multiple lienholders share reductions proportionally rather than being paid in strict priority order.

How Attorneys Negotiate Lien Reductions

One of the most valuable services a personal injury attorney provides is negotiating reductions in medical liens. Successful lien negotiation can dramatically increase the net amount you receive from your settlement. Attorneys use several strategies to reduce liens:

The Made Whole Doctrine

Many states recognize the “made whole” doctrine, which holds that an injured person must be fully compensated for all their losses before a subrogation lien can be enforced. If your settlement doesn’t make you whole—meaning it doesn’t fully compensate you for all economic and non-economic damages—your attorney can argue that the lien should be reduced or eliminated.

For example, if your total damages (medical bills, lost wages, pain and suffering) equal $300,000 but you settle for $150,000, you’ve only been made 50% whole. Under the made whole doctrine, lienholders should accept proportional reductions or possibly receive nothing until you’re fully compensated.

The Common Fund Doctrine

The common fund doctrine recognizes that your attorney’s work in recovering the settlement created the fund from which lienholders will be paid. Under this doctrine, lienholders should contribute to the attorney’s fees and costs that made the recovery possible. This typically results in reducing the lien by the percentage of attorney’s fees (often 33-40%) and sometimes litigation costs as well.

Using our earlier example, if a health insurer claims a $50,000 subrogation lien but your attorney worked on contingency for 33%, the common fund doctrine would reduce the lien by $16,500, leaving only $33,500 owed to the insurer.

Challenging Unrelated Charges

Attorneys carefully review lien claims to identify charges unrelated to the accident. Liens should only cover treatment for injuries caused by the incident in question. If a hospital lien includes charges for pre-existing conditions or unrelated treatment, those amounts should be disputed and removed.

Negotiating Reasonable Amounts

For hospital liens based on chargemaster rates, attorneys negotiate for more reasonable amounts that reflect what insurers typically pay. Many hospitals will accept substantial reductions when faced with the alternative of costly litigation or potentially receiving nothing if the settlement is exhausted by other liens.

Leveraging Statutory Protections

In states with laws limiting subrogation or lien recovery, attorneys use these protections to negotiate better outcomes. Some states prohibit subrogation entirely in cases where the settlement doesn’t fully compensate the injured party. Others require liens to be reduced proportionally based on the settlement amount compared to total damages.

Working With Multiple Lienholders

When multiple liens exist, attorneys often negotiate with all lienholders simultaneously, demonstrating that the settlement funds are limited and encouraging each lienholder to accept reductions so that everyone receives something. This approach can result in better overall outcomes than negotiating sequentially.

Practical Considerations for Settlement Recipients

Understanding medical liens helps you navigate the settlement process more effectively. Here are key considerations:

Don’t Ignore Liens: Attempting to settle without addressing liens can result in lawsuits from lienholders, personal liability, and other serious consequences. Always identify and address all liens before finalizing a settlement.

Document Everything: Keep detailed records of all medical treatment, bills, insurance payments, and communications. This documentation is essential for evaluating and disputing liens.

Allow Time for Resolution: Lien resolution takes time, often several months. Don’t expect immediate payment after settling your case. Medicare alone can take 60-90 days or longer to process a final demand.

Set Realistic Expectations: Understand that liens may substantially reduce your net recovery. Your attorney should provide realistic estimates of what you’ll receive after liens are satisfied.

Consider Liens in Settlement Negotiations: The amount you’ll actually receive after satisfying liens should influence whether to accept a settlement offer. A $100,000 settlement might only net you $40,000 after liens, making it less attractive than it initially appears.

Medical liens represent a complex but crucial aspect of personal injury settlements. Whether dealing with health insurance subrogation, hospital liens, or Medicare and Medicaid recovery, understanding who has claims against your settlement and how those claims are resolved is essential to maximizing your recovery.

Experienced personal injury attorneys add substantial value through their ability to identify all liens, negotiate meaningful reductions, and ensure the maximum amount possible ends up in your pocket. While liens may reduce your settlement, proper handling can significantly minimize their impact and help ensure you receive fair compensation for your injuries.

If you’re pursuing a personal injury claim, work with an attorney who has extensive experience handling medical liens. Their expertise in lien negotiation may ultimately determine whether your settlement provides adequate compensation or leaves you struggling to cover your ongoing expenses.