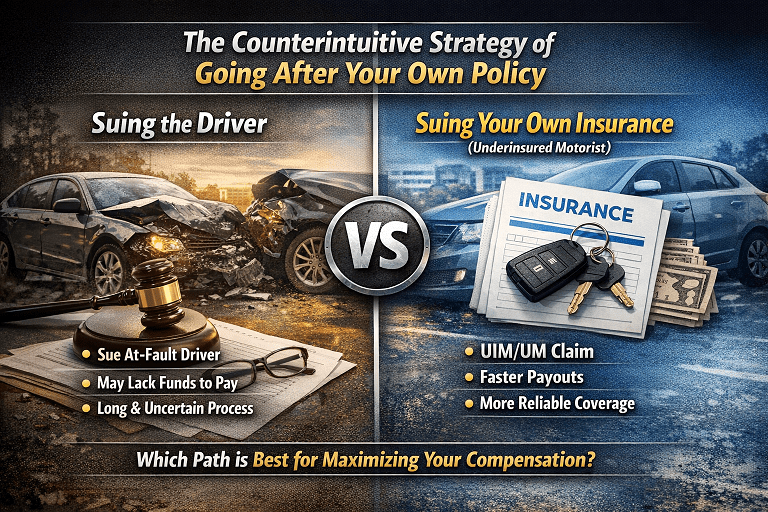

Underinsured Motorist: The Counterintuitive Strategy of Going After Your Own Policy

When you’re injured in a car accident caused by another driver, your first instinct might be to pursue the at-fault driver directly for compensation. This seems logical—they caused the accident, so they should pay for your damages. However, there’s a counterintuitive strategy that accident victims and their attorneys often employ: filing a claim against your own insurance policy through uninsured motorist (UM) or underinsured motorist (UIM) coverage. This approach can be more effective, faster, and more reliable than chasing an individual driver who may lack the financial resources to compensate you adequately.

Understanding this strategic choice requires examining both options, their advantages and disadvantages, and the circumstances under which pursuing your own insurance makes better sense than suing the at-fault driver directly.

Understanding Uninsured and Underinsured Motorist Coverage

Before diving into strategy, it’s essential to understand what UM and UIM coverage actually provides. These coverage types are add-ons to your auto insurance policy designed to protect you when the at-fault driver either has no insurance or insufficient insurance to cover your damages.

Uninsured motorist coverage applies when the at-fault driver has no insurance, while underinsured motorist coverage helps when the other driver’s liability limits are too low to fully cover your losses. These coverages essentially allow your own insurance company to step into the shoes of the at-fault driver’s insurer and compensate you for medical expenses, lost wages, pain and suffering, and other accident-related damages.

In most cases, your uninsured or underinsured motorist coverage limits cannot exceed your liability coverage limits. For example, if you carry liability coverage with policy limits of fifty thousand dollars, you typically cannot purchase more than fifty thousand dollars in UM or UIM coverage. This linkage means that higher liability coverage also provides better protection for yourself.

The coverage works differently depending on whether the driver is uninsured or underinsured. With an uninsured driver, you can file a UM claim directly with your own insurer from the outset. With an underinsured driver, the process is more complex—you typically must first exhaust the at-fault driver’s liability coverage before your UIM coverage kicks in to cover the remaining damages.

The Prevalence of Uninsured and Underinsured Drivers

Approximately eight percent of drivers throughout the United States don’t have any insurance coverage, and that number can be much higher in some states. This statistic alone highlights why UM and UIM coverage is so valuable. Even if you’re a careful driver who follows all traffic laws, you cannot control whether other drivers maintain proper insurance.

Furthermore, many states have minimum liability insurance requirements that are shockingly low—sometimes as little as twenty-five thousand or fifty thousand dollars per person. When you consider that a single emergency room visit can cost thousands of dollars, and serious injuries involving surgery, rehabilitation, and lost wages can easily exceed one hundred thousand dollars or more, these minimum coverage amounts are often woefully inadequate.

This creates a situation where even insured drivers may be functionally “underinsured” relative to the damages they cause. A driver with the state minimum coverage who causes a catastrophic accident resulting in hundreds of thousands of dollars in damages leaves a substantial gap between their policy limits and the victim’s actual losses.

The Challenge of Suing an Uninsured or Underinsured Driver Directly

When the at-fault driver lacks insurance or has insufficient coverage, you have the legal right to file a personal injury lawsuit against them individually. If successful, the court will issue a judgment ordering the driver to pay your damages. However, obtaining a judgment is only half the battle—the real challenge lies in collecting that money.

The Collection Problem

A judgment is ultimately a piece of paper that does not magically put money into your bank account, and the difficult next step is to enforce that judgment by finding a way to collect the money from the person who owes it legally.

Many times the reason a driver doesn’t have car insurance is because they can’t afford it or have accidentally let their insurance lapse. If a driver cannot afford insurance premiums, they’re unlikely to have significant assets that could satisfy a substantial judgment. Even if you win your case in court, you may recover little or nothing if the defendant has limited income and no substantial assets.

Enforcement mechanisms exist, including wage garnishment, property liens, and asset seizure, but these tools are only effective if the defendant has wages to garnish or assets to seize. If the driver has no significant assets, is unemployed, or files for bankruptcy, collection can be extremely difficult. Bankruptcy, in particular, can discharge many personal injury judgments, leaving you with nothing despite your legal victory.

The Time and Expense of Litigation

Filing a lawsuit involves significant time and expense. You’ll need to pay court filing fees, potentially hire expert witnesses, and dedicate months or even years to the litigation process. Most personal injury attorneys work on contingency fees, meaning they take a percentage of your recovery—typically thirty to forty percent. If the defendant has no assets, attorneys may be less willing to take your case on contingency, requiring you to pay hourly or flat fees upfront regardless of the outcome.

When your losses are fully covered by UM or MedPay, you might recover more through insurance than litigation, as legal fees and time spent might outweigh what you’d collect, especially in smaller claims.

When Suing the Driver Makes Sense

Despite these challenges, directly suing the at-fault driver does make sense in certain circumstances. If you can verify that the driver has significant assets—such as property ownership, a steady high-income job, or substantial savings—pursuing litigation becomes more viable. Your attorney can conduct asset searches, review public records for property deeds, and investigate the defendant’s financial situation before investing time and resources into a lawsuit.

An experienced car accident attorney can run an asset and credit check on the driver to establish their financial standing, and may recommend filing a lawsuit if the assessment shows the driver is financially stable. Additionally, if your damages significantly exceed your UM or UIM policy limits and the defendant has recoverable assets, filing a lawsuit to recover the difference may be your only option for full compensation.

Another scenario involves placing liens on the defendant’s property. You can file for a lien on the uninsured driver’s property, which will mean their assets become frozen and cannot be sold or spent, and you must be paid if they sell the property. This strategy essentially creates a waiting game where you’ll eventually collect when the property is sold, though it may take years.

The Advantages of Filing a UM/UIM Claim Against Your Own Insurance

Given the challenges of pursuing an uninsured or underinsured driver directly, filing a claim under your own UM or UIM coverage often presents a superior alternative. This approach offers several significant advantages that make it the preferred strategy in most cases.

Contractual Obligation and Reliability

When you file a UM claim, you deal with your insurer, and your insurance company has a contractual obligation to pay you under the terms of your policy, whereas an uninsured individual has no such relationship with you. This contractual duty creates a more reliable path to compensation than chasing an individual who may have no means to pay.

You’ve paid premiums specifically for this protection. Your insurance company promised to cover you in exactly this situation—when an at-fault driver cannot adequately compensate you for your injuries. This makes UM and UIM coverage fundamentally different from pursuing a third party with no legal obligation to you beyond general tort liability.

Streamlined Process

A UM claim is designed to be a more streamlined process than a full-blown lawsuit that could drag on for years through the court system. Claims involving at-fault drivers with no insurance at all tend to be fastest because there is no other party or insurance company to deal with, as the claimant can just submit the claim directly to their own insurance company.

While UM and UIM claims still involve investigation, negotiation, and potentially arbitration, they generally resolve faster than civil litigation. Your insurer has established claims processes, adjusters familiar with these claims, and incentives to resolve matters within reasonable timeframes to avoid bad faith allegations.

Coverage for Full Spectrum of Damages

By making a UIM claim with your own car insurance company, you can receive compensation for the entire spectrum of your car accident-related losses, just as you would if the at-fault driver did have insurance.

With an uninsured motorist claim, you can usually receive compensation for the same kinds of injury-related losses that you might get in a liability claim against the at-fault driver, including payment for past medical treatment, payment to cover costs of future medical care, reimbursement of lost income, and compensation for physical and mental pain and suffering.

This comprehensive coverage means you’re not settling for less just because you’re dealing with your own insurer rather than the at-fault driver. The damages recoverable under UM and UIM claims mirror those available in third-party liability claims.

No Premium Increase

A common concern about filing claims against your own insurance is whether it will increase your premiums. Georgia law prohibits your UIM carrier from raising your insurance rates simply for making a claim when the accident is not your fault. In many states, filing an uninsured motorist claim for an accident that was clearly not your fault should not cause your premiums to increase, as these claims are intended to protect you when the at-fault driver lacks insurance.

While insurance company practices vary and some may factor claims into renewal pricing, laws in many states protect policyholders from rate increases due to no-fault UM and UIM claims. This removes a significant barrier that might otherwise discourage people from using coverage they’ve paid for.

Avoiding Bankruptcy Issues

When you sue an individual driver, they can potentially discharge the debt through bankruptcy, leaving you without compensation despite your legal victory. Insurance companies, by contrast, cannot simply declare bankruptcy to avoid paying valid claims. They’re regulated entities required to maintain reserves and demonstrate financial solvency. This makes recovery far more certain when dealing with an insurer than an individual defendant.

The Downsides and Limitations of UM/UIM Claims

While UM and UIM coverage offers substantial advantages, the strategy isn’t without limitations and potential drawbacks that accident victims should understand.

Policy Limits Cap Recovery

The most significant limitation is that your recovery is capped at your policy limits. If you carry UM/UIM coverage with limits of one hundred thousand dollars but suffer damages totaling three hundred thousand dollars, your own insurance will only pay up to the policy maximum. The total amount you can get from an uninsured motorist claim hinges on the dollar limits of your uninsured motorist coverage.

In contrast, a lawsuit against a wealthy defendant with substantial assets could potentially recover the full amount of your damages, regardless of how high they might be. This makes lawsuits against financially capable defendants potentially more valuable for catastrophic injury cases with damages exceeding your policy limits.

Arbitration Instead of Lawsuit Rights

One very important difference between a claim against the at-fault driver and a UIM claim filed with your own insurance company is that if you and your insurer cannot agree on a fair settlement figure, you probably won’t be able to file a lawsuit against your insurer; instead, you’ll likely have to submit your claim to binding arbitration.

Arbitration is a more informal procedure than a court trial and can limit your rights if you disagree with the outcome. Unlike court judgments, arbitration decisions typically offer very limited appeal rights, meaning you’re generally stuck with the arbitrator’s decision even if you believe it’s unjust. This restriction can be particularly frustrating for claimants who feel their damages have been undervalued.

Your Insurer Is Not Your Friend

A critical misunderstanding many policyholders have is believing their own insurance company will be on their side during a UM or UIM claim. It’s important to remember that your insurance company will fight the claim, and it is best if you treat them as your adversary. Even when dealing with adjusters from your own insurance company, you should not assume they are on your side, as insurance companies will do anything they possibly can to undervalue a claim.

Your insurer has a financial incentive to minimize what they pay out on your claim, just as they would with any claim. They will investigate your medical treatment, question the extent of your injuries, and seek to settle for the lowest amount possible. This adversarial dynamic can feel particularly frustrating when you’ve been paying premiums to this company for years.

Proving Fault Remains Necessary

Even when suing your own insurer, you must show that the uninsured or underinsured driver caused the crash and that you’re entitled to compensation under your policy. You cannot simply file a claim because you were in an accident—you must still prove the other driver was at fault and that their negligence caused your injuries.

This requires gathering evidence, obtaining police reports, securing witness statements, and demonstrating the elements of negligence: duty of care, breach of that duty, causation, and damages. The burden of proof remains on you, the claimant, even though you’re dealing with your own insurance company.

Coordination with Third-Party Settlements

When dealing with an underinsured driver, the process becomes more complex because you typically must first exhaust the at-fault driver’s policy limits before accessing your UIM coverage. This coordination requirement can delay your claim and complicate settlement negotiations.

For example, if the at-fault driver has liability coverage of fifty thousand dollars and you have UIM coverage of one hundred thousand dollars, you would need to settle with the at-fault driver’s insurer for their full policy limits before your UIM coverage would pay the additional amount needed to reach your total damages or your UIM policy limits, whichever is less.

Insurance Bad Faith: A Powerful Enforcement Tool

One of the most powerful protections available to policyholders pursuing UM or UIM claims is the legal doctrine of insurance bad faith. This doctrine recognizes that insurance companies have special obligations to their policyholders beyond what they owe to third parties.

The Duty of Good Faith and Fair Dealing

Every insurance contract contains an implied covenant of good faith and fair dealing. Insurance companies are legally required to deal with policyholders fairly in an effort to resolve claims, and this is especially true when it comes to your own insurance company, which has an obligation to act in good faith when carrying out its duties under your policy.

This duty means your insurer must give at least as much consideration to your interests as it gives to its own interests. When an insurer unreasonably and in bad faith withholds payment, denies a claim without proper investigation, or drastically undervalues a legitimate claim, they can be held liable for damages beyond the original policy limits.

What Constitutes Bad Faith

An insurance company’s actions can be deemed in bad faith if they are found to be unreasonable or without proper cause. Common examples of bad faith conduct in UM and UIM claims include:

- Unreasonably denying a valid claim without legitimate justification

- Failing to properly or promptly investigate the facts of your claim

- Unreasonably delaying payment or settlement of a valid claim

- Making lowball settlement offers that bear no reasonable relationship to the actual value of your claim

- Requesting excessive or unnecessary documentation to create delays

- Misrepresenting policy terms to avoid paying a claim

- Failing to communicate or explain claim decisions

An adjuster for your own insurance company is not negotiating in bad faith just because you and the adjuster have a difference of opinion about how much your claim is worth; however, bad faith may exist if the adjuster has refused to give you any specific reasons for a very low settlement offer or has engaged in improper settlement tactics.

Damages for Bad Faith

The potential consequences for insurance companies that act in bad faith can be severe. When an insurer’s refusal to pay a claim is vexatious and unreasonable, the insured may be entitled to additional damages and their attorney’s fees, and there are no limits on a bad faith insurance claim even if the value of a particular claim exceeds the limits of the subject insurance policy.

This means that while your UM or UIM coverage might have limits of one hundred thousand dollars, a successful bad faith claim could potentially recover significantly more to compensate you for the insurer’s misconduct. Bad faith damages can include the original policy benefits that should have been paid, consequential damages resulting from the denial or delay, emotional distress damages, punitive damages to punish egregious conduct, and attorney’s fees.

Strategic Implications

The existence of bad faith liability creates powerful incentives for insurance companies to handle UM and UIM claims reasonably. A written accusation of bad faith often gets prompt attention and, if justified, may rapidly provoke a change in the insurance adjuster’s settlement position. Even if proving bad faith in court is difficult, the mere possibility of a bad faith claim can help nudge a reasonable settlement offer from an insurance company during negotiations.

For accident victims, understanding bad faith principles provides important leverage in dealing with their own insurers. If your insurer is acting unreasonably—refusing to explain low offers, ignoring evidence of your injuries, or delaying without justification—consulting with an attorney experienced in bad faith claims can help protect your rights and potentially increase your recovery substantially.

Strategic Considerations: Choosing Your Path

Given the advantages and limitations of both approaches, how should accident victims decide whether to pursue the at-fault driver directly, file a UM or UIM claim with their own insurer, or potentially pursue both avenues?

Assessing the At-Fault Driver’s Financial Situation

The threshold question is whether the at-fault driver has recoverable assets. If the driver is judgment-proof—meaning they have no significant income, property, or other assets that could satisfy a judgment—pursuing them directly is likely a waste of time and resources regardless of how strong your liability case might be.

Your attorney can investigate the driver’s financial situation through public records searches, property ownership verification, employment status investigation, and credit checks. This investigation should happen early in the process, ideally before investing significant resources in litigation against an individual who cannot pay.

Evaluating Your UM/UIM Coverage

Review your own insurance policy carefully to understand your UM and UIM coverage limits. If your coverage is sufficient to cover most or all of your damages, pursuing your own insurer is likely the more efficient path. If your damages substantially exceed your policy limits and the at-fault driver has recoverable assets, you may need to pursue both avenues—settling with your own insurer for your policy limits and suing the driver for the difference.

Considering the Complexity of Your Claim

For straightforward claims with clear liability and well-documented damages falling within your policy limits, filing a UM or UIM claim typically makes sense. The streamlined process will resolve your claim faster and with less expense than litigation.

For complex cases involving disputed liability, catastrophic injuries with ongoing medical needs, or damages far exceeding available insurance coverage, the calculus becomes more complicated. These cases often benefit from the expertise of an attorney who can evaluate all potential recovery sources and develop a comprehensive strategy.

Timing Considerations

You generally have one year from the accident date to file a UM claim, but deadlines vary by state. Personal injury lawsuits also have statutes of limitations, typically two to three years depending on the state. These deadlines create time pressure for decision-making.

It’s important to preserve your rights under both potential avenues early in the process. You can notify your own insurer of the accident and begin the UM or UIM claims process while simultaneously investigating whether pursuing the at-fault driver directly makes sense. Early notification also prevents potential coverage issues—some insurance policies require reporting accidents within very short timeframes, sometimes as brief as thirty days.

The Combined Approach

In many cases, the optimal strategy involves pursuing both avenues simultaneously or sequentially. For an underinsured driver with some coverage, you would typically first pursue the at-fault driver’s liability insurance to obtain their policy limits, then file a UIM claim with your own insurer to cover the gap between that recovery and your total damages.

Cases involving underinsured drivers usually take longer to settle because the primary claim against the at-fault driver needs to be resolved first before the UIM claim can be finalized.

If the at-fault driver has assets beyond their insurance coverage and your damages exceed your UM or UIM policy limits, you might settle with your own insurer for your policy maximum and then pursue the driver individually for additional damages. This stacking of recoveries can maximize your total compensation.

The Importance of Legal Representation

Whether you choose to pursue the at-fault driver, file a UM or UIM claim, or both, navigating these claims effectively typically requires experienced legal representation. The insurance claims process is complex, and mistakes can substantially reduce your recovery or even eliminate your rights entirely.

Specialized Knowledge

Lawyers frequently handle cases against UM carriers, as state laws have special rules for UM claims. These special rules can include unique statutes of limitations, specific notice requirements, mandatory arbitration provisions, and complex coordination-of-benefits rules when multiple insurance policies are involved.

An attorney experienced in UM and UIM claims understands these nuances and can help you avoid procedural pitfalls that could jeopardize your claim. They can also accurately value your claim by understanding the full scope of recoverable damages, including future medical expenses, ongoing care needs, and long-term wage loss that you might not immediately recognize.

Leveling the Playing Field

Even though you are filing a claim with your own insurer, their primary goal is to pay as little as possible. Insurance companies have teams of adjusters, attorneys, and experts working to minimize what they pay on claims. Having your own attorney creates more balance in this inherently adversarial process.

Your attorney can gather and organize evidence effectively, obtain expert opinions to support your damages, negotiate from a position of knowledge rather than weakness, and recognize when an insurer is acting in bad faith. This professional advocacy significantly increases the likelihood of obtaining fair compensation.

Contingency Fee Arrangements

Most personal injury attorneys, including those handling UM and UIM claims, work on contingency fees. This means you pay no attorney’s fees unless your attorney recovers compensation for you. The attorney’s fee comes as a percentage of the recovery, typically thirty to forty percent.

While this percentage might seem substantial, studies consistently show that accident victims represented by attorneys recover significantly more on average than those who handle claims themselves, even after deducting attorney’s fees. The attorney’s expertise in valuation, negotiation, and claim presentation typically more than justifies their fee.

Recognizing When You Need Help

Some accident victims attempt to handle UM or UIM claims themselves, particularly for smaller claims with clear liability and straightforward damages. While this is possible, warning signs that you need professional help include:

- The insurance company has denied your claim

- The settlement offer seems unreasonably low relative to your damages

- Your injuries are serious or have lasting effects

- The insurance company is requesting excessive documentation or creating delays

- Liability is disputed

- Multiple insurance policies might provide coverage

- Your damages exceed the available insurance coverage

In these situations, the cost of not having an attorney—in terms of undervalued claims, procedural mistakes, or missed opportunities—typically far exceeds the cost of hiring one.

Maximizing Your UM/UIM Coverage

Given the importance of UM and UIM coverage, it’s worth discussing how to ensure you have adequate protection before an accident occurs.

Reviewing Your Coverage Regularly

Many people purchase auto insurance without carefully reviewing their coverage options, accepting minimum liability limits and declining optional coverages to save money on premiums. This penny-wise, pound-foolish approach leaves you vulnerable when an uninsured or underinsured driver injures you.

Individuals should opt for high UIM and UM coverage limits because Georgia has low minimum auto insurance requirements, UIM coverage is generally fairly affordable, and you may need this additional coverage in the event of an accident. This principle applies nationwide, not just in Georgia. The relatively small premium difference between minimum and more robust coverage can mean the difference between full compensation and financial devastation after a serious accident.

Matching Liability and UM/UIM Limits

Insurers do not want people purchasing bare bones coverage for their own liability and loading up on uninsured/underinsured motorist coverage. As a result, most policies link your UM and UIM coverage limits to your liability coverage limits, often capping UM/UIM at the same level as your liability coverage.

This linkage creates a simple rule of thumb: increase your liability coverage, and you’ll automatically increase the protection available to you through UM and UIM coverage. If you carry liability limits of one hundred thousand dollars per person, consider increasing to three hundred thousand dollars or five hundred thousand dollars. This protects both others if you cause an accident and yourself if an uninsured or underinsured driver injures you.

Understanding State Requirements

UM and UIM coverage requirements vary dramatically by state. Some states require insurance companies to offer these coverages, while others mandate that all policies include them unless you specifically opt out in writing. If you are a Georgia resident with auto insurance for the state of Georgia, you likely have uninsured/underinsured motorist coverage unless you specifically signed a document opting out when you purchased your policy.

Unfortunately, many people sign these opt-out forms without understanding what they’re giving up, often at the encouragement of insurance agents looking to reduce premiums. Later, after an accident with an uninsured driver, they discover they have no coverage for their injuries—a devastating realization that could have been avoided with proper understanding.

Review your policy declarations page or contact your insurance agent to verify whether you have UM and UIM coverage, what the limits are, and whether you’ve opted out of any available coverage. If you’ve opted out or have minimal coverage, seriously consider increasing your protection.

The Counterintuitive Makes Sense

The strategy of pursuing compensation from your own insurance company rather than the at-fault driver seems counterintuitive at first glance. You’ve been paying premiums to your insurer for years, and now when you need help, you must essentially fight with your own company for compensation. Meanwhile, the person who actually caused your injuries might escape with minimal financial consequences.

Despite this uncomfortable reality, the strategy makes sense from a practical standpoint. Your own insurer has a contractual obligation to pay valid claims, financial resources to satisfy those obligations, and legal vulnerabilities through bad faith doctrine if they act unreasonably. An uninsured or underinsured at-fault driver, by contrast, may have none of these things—no obligation beyond general tort liability, no resources to pay a judgment, and no fear of regulatory consequences or bad faith liability.

The key is understanding when to use each strategy. For catastrophic injuries with damages substantially exceeding your policy limits where the at-fault driver has significant recoverable assets, pursuing the driver directly makes sense. For most other scenarios—particularly when dealing with truly uninsured drivers or underinsured drivers with minimal assets—your UM or UIM coverage provides the most reliable path to fair compensation.

This reality underscores the critical importance of purchasing adequate UM and UIM coverage before an accident occurs. While you cannot control whether other drivers maintain proper insurance, you can ensure you have protection when they don’t. The relatively modest additional premium for robust UM and UIM coverage is one of the best insurance investments you can make, potentially saving you from financial catastrophe after a serious accident with an uninsured or underinsured motorist.

Ultimately, the counterintuitive strategy of going after your own insurance company reflects the broader reality of accident compensation in America: insurance, not individual liability, drives most recoveries. Understanding this reality and ensuring you have proper coverage is essential to protecting yourself and your family on the road.